Building 34, No. 535 Shunfeng Road, Hangzhou, Zhejiang, China

[email protected]

Renewable energy storage costs refer to the total cost to store wind or solar power, ranging from battery hardware and controls to grid tie-in, labor, and long-term service. Costs keep dropping, but they still determine which projects progress, what capacity gets constructed, and how quickly plants can retire fossil backup. These key drivers encompass battery chemistry, energy density, cycle life, and balance-of-plant gear such as power converters, chillers, and switchgear. Grid rules, tariffs, and peak pricing alter the actual cost per kWh stored. For plant and facility teams, storage cost now ties directly to power quality, uptime, and long-term energy spend. The following sections dissect these cost blocks in greater depth.

Renewable storage cost is not a number. It’s a stack of capital, performance, risk and lifetime decisions that unfold over 10 to 20 years. For plant teams planning massive loads, such as paint lines, cleanrooms, or data halls, the trick is to examine total cost of ownership, not just the cost of the battery or thermal tank on day one.

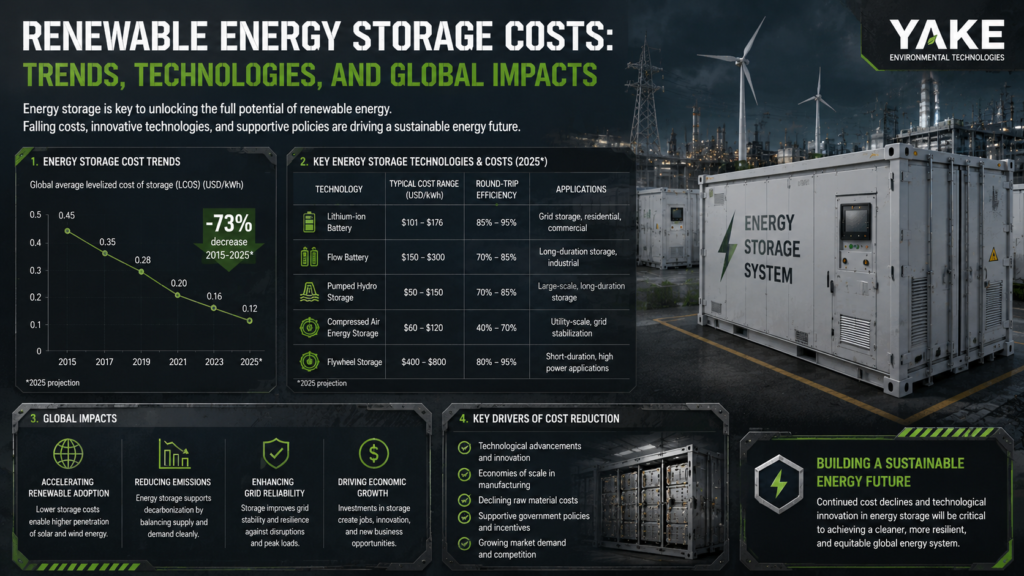

Different storage technologies have different cost profiles. Lithium-ion has spearheaded cost declines. Pack prices declined nearly 90% by 2020, which helped drive broad solar-plus-storage adoption. Pumped hydro is inexpensive per kilowatt-hour at scale but requires unique locations. Flow batteries and compressed-air systems offer long duration potential but remain in nascent commercialization phases, meaning they carry high capital expenditure and project risk.

Round‑trip efficiency is just as important as sticker price. Lithium‑ion often runs 88 to 92 percent efficient, while a few long‑duration and thermal variants beat in the 50 to 75 percent range. Lower efficiency means you have to oversize both the storage itself and the upstream solar or wind to deliver the same kilowatt-hours, which increases system cost.

Technology maturity drives financing terms. Bankable, proven systems get better interest rates, longer debt, and better warranties. That slices LCoS even if their capex is not the absolute lowest.

New possibilities such as iron‑air batteries, high‑temperature thermal storage, and advanced hydrogen are willing to exchange lower energy density in return for inexpensive, abundant materials and ultra long duration. If they scale up, they might drive long duration storage costs down the way lithium‑ion batteries and solar panels dropped 85% in price after scaling up in the early 2000s.

Because it’s made of raw materials, it ties storage costs to truly global commodity cycles. Lithium, cobalt, nickel, and copper account for the majority of the cost of lithium-ion systems, while vanadium can dominate flow batteries. Rare or geographically concentrated resources introduce price spikes and supply risk.

Recycling and second-life use contribute. Reclaiming lithium, cobalt, and copper can reduce net material cost and stabilize supply, while repurposing EV packs as stationary storage defers new cell demand.

| Storage type | Key materials |

|---|---|

| Lithium‑ion battery | Lithium, cobalt/nickel, graphite, copper, aluminum |

| Flow battery | Vanadium or zinc‑bromine, polymer membranes |

| Pumped hydro | Concrete, steel, earthworks |

| Hydrogen storage | Steel, composites, platinum‑group catalysts |

Cost per kWh typically declines as systems scale. Large battery containers, shared inverters, and common balance of plant spread fixed engineering and grid tie costs over many more kWh. Gigafactories take this further. Mass production pushes unit prices down through learning curves and supply chain deals.

Scaling to grid level doesn’t come for free. Big battery sites need high‑voltage interconnects, land, permits, and sometimes grid upgrades. Small behind‑the‑meter systems sidestep some of that, but hardware and install cost per kWh remain higher.

For industrial users, co-located solar and four-hour battery blocks can now meet a lion’s share of site or data-center load more cheaply than gas in sunny regions with high power prices. In many European markets, declining storage costs already make solar-plus-storage economically compelling, not just a “green” option.

Lifetime shifts total cost further than most budgets acknowledge. Cycle life, calendar life, and degradation rate determine how much usable energy you return from the same capex. A lower-priced system that requires swap-out in 7 years can end up more expensive than a higher-priced unit that operates 15 years with gradual fade.

Lithium-ion commonly guarantees 60 to 70 percent capacity retention after 10 years. Certain long-duration chemistries aim for over 20 years with reduced annual fade and increased initial cost. Maintenance is uneven: pumped hydro and mechanical systems need more regular service, while sealed batteries look simpler but may need full module change-out.

Warranties, performance guarantees, and transparent degradation curves are important inputs to LCOE. They assist in modeling future capital expenditure hits and operational and maintenance costs. That matters as solar and battery LCOE are expected to fall another approximately 30% and 25% by 2035, which will drive more buyers to care about lifetime cost, not just capital expenditure.

Where you locate storage moves both costs and value. Land price, grid-tie distance, and local labor rates influence install cost. Climate plays a part: very hot or humid sites need tighter thermal and humidity control to protect battery life and safety, which adds HVAC and dehumidification loads but can prevent early failure.

Being close to both generation and load reduces cable runs, trenching and substation work. With one-time fees on the grid, on-site systems at factories or data centers, for instance, sidestep some grid charges and can leverage on-site solar, crucial as volume-based grid tariffs stress. Others predict as much as a 38% decline in grid demand when lots of homes install solar and storage.

Remote projects encounter road access, shipping, and service crew expenses. They require sturdier climate enclosures. That’s where stable indoor conditions, such as dry air and narrow temperature bands, become a cost lever since better climate cuts degradation and fire risk and extends battery life.

Declining storage prices are already causing early adopters’ sustainability goals to overlap with simple cost savings. As battery storage reaches record-low costs while some other cleantech prices increase, an increasing number of future users will purchase storage first to reduce bills and then appreciate resilience and carbon reductions as a bonus.

Cost comparison starts with the service stack each asset can deliver: peak shaving, firming renewables, black start, inertia, fast frequency response, or seasonal shifting. Storage should be compared, for a level playing field, by mapping it in a 3-D matrix of power (MW), energy (MWh), and duration. It should then be benchmarked against response times (10%, 50%, 100% output), self-discharge (1 day to 1 year), and usable depth of discharge. The table below provides representative utility-scale price bands for a 60 MW, 480 MWh case.

| Technology | Capex (€/kW) | Capex (€/kWh) | Fixed Opex (%/yr) | Round‑trip η | Typical Life (years/cycles) |

|---|---|---|---|---|---|

| Li‑ion battery | 400–900 | 150–350 | 1–3 | 85–92% | 10–15 / 3,000–8,000 |

| Flow battery | 600–1,200 | 80–200 | 1–3 | 70–85% | 15–20 / 10,000+ |

| Pumped hydro (PHS) | 1,000–3,000 | 20–60 | 1–2 | 75–85% | 50–80 / n.a. |

| Hydrogen (H2-CCGT-R) | 700–1,500 | 10–40 | 2–4 | 30–45% | 25–35 / n.a. |

| CAES / PTES | 600–1,500 | 10–80 | 2–4 | 45–70% | 25–40 / n.a. |

| Flywheel | 800–2,000 | 500–3,000 | 2–5 | 85–95% | 20+ / 100,000+ |

Cost strengths differ. Batteries win for short-duration, high-value grid services. Pumped hydro and PTES work for day-scale bulk storage where sites exist. Hydrogen and a few mechanical candidates catch traction again as soon as you require multi-day or seasonal coverage and fuel storage volume means more than round-trip efficiency.

Lithium-ion dominates 1 to 4 hour storage. Capital expenditure is still dropping but is now flattening as materials costs rise. Flow batteries, sodium-based systems, and high-temperature liquid-metal designs all sit higher on capital expenditure today, but all scale energy in kilowatt-hours cheaper than power in kilowatts, which helps as you push beyond 6 to 8 hours. High-temperature chemistries also bring a special cost line item. They must stay near or above 300 degrees Celsius to keep active materials liquid, so standby heat demand shows up in operating expenses and in self-discharge over days and weeks.

Cycle life and round-trip efficiency help LCOS go down. A lithium-ion pack that’s 90% efficient, good for 6,000 full cycles, and operates at an 80% depth-of-discharge distributes capex across countless arbitrage and grid-service events. A flow battery could provide over 10,000 cycles at 70 to 80% efficiency, so despite higher euros per kilowatt pricing, cost per megawatt-hour throughput is flat or lower for long duty cycles. Short cycle life, limited depth-of-discharge, and rising resistance all drive LCOS higher.

Recycling is now a key economic lever. Closed-loop lithium-ion recycling recovers nickel, cobalt, lithium, and copper and cuts raw materials exposure. This can translate into a lower end-of-life net cost, particularly if metal shortage inflates spot prices. It aids in tackling ethical concerns about mining and supply from high-risk areas. Flow systems depend more on abundant elements, so they experience less volatility but still require recycling schemes for electrolytes and membranes.

Upfront battery cost is steep. PCS, HVAC, fire systems, and controls sit on top of cells and racks. Ongoing costs are non-trivial as well. Augmentation to offset degradation, periodic inverter replacement, safety inspections due to fire and thermal-runaway risk, and cooling or heating energy are all necessary. For industrial users pursuing rapid response services, batteries often triumph on revenue density per installed euro, but are still pricey for low-value, multi-day storage unless bundled with a bunch of services simultaneously.

Pumped hydro uses mature civil works and standard electro-mechanical equipment, so equipment capex per kWh is low. The total bill is large because of dams, tunnels, and land. Fixed opex is modest in comparison to capex. Variable opex is primarily water losses and auxiliary power. This architecture implies pumped hydro works optimally where a grid can maintain it at an elevated capacity factor for decades.

Site requirements push viability over tech cost. You need two substantial reservoirs that have enough height difference, stable geological conditions, water supply, and social and environmental acceptability. Lots of potential valleys are remote from renewable build-out zones or have severe land-use constraints, which adds queues and increases actual project cost.

The economic upside is longevity and predictable performance. Assets can run 50 to 80 years with refurbishments, and round-trip efficiency stays still. Operating staff requirements and maintenance are low per MWh stored. Pumped hydro typically delivers the lowest levelized cost of storage among other large-scale options for 4 to 48 hour storage where sites exist and offers inertia and fast frequency response in addition to bulk shifting. For one to several day needs, pumped hydro, PTES, and hydrogen in retrofitted gas turbines frequently find themselves in a close race, with local geography and fuel price tipping the outcome.

Hydrogen storage breaks into three big cost blocks: production by electrolysis, storage in tanks, caverns, or pipelines, and power conversion back to electricity in a turbine or fuel cell. Electrolyzers are still capital expenditure heavy, and round trip efficiency from power to hydrogen to power often lands in the 30 to 45 percent range, so every loss goes straight onto levelized cost of storage. Storage media costs vary: steel tanks are expensive but simple, and underground salt caverns are cheaper per kilowatt-hour but only possible in some regions.

Infrastructure and transport tend to rule real project economics. Pipelines, compressors and safety systems require significant up-front investment and careful siting in proximity to loads or existing gas networks. Transport of hydrogen by truck or ship adds compression, liquefaction or conversion losses. These factors can dwarf equipment costs in early projects and strongly influence whether hydrogen operates as centralized bulk storage or more local backup.

Cost trajectories are being reshaped by electrolysis manufacturing scale-up, turbine makers shipping hydrogen-ready CCGT units, and burgeoning policy support. Learning curves indicate falling electrolyzer and fuel cell prices and improved efficiency that can close some of the gap with batteries and pumped hydro, particularly for long-duration use where hydrogen’s low storage volume cost outweighs round-trip losses. For multi-day to seasonal storage, hydrogen can undercut batteries on euros per megawatt-hour of storage capacity, while still remaining more costly in delivered megawatt-hours due to losses.

Relative to today’s batteries and pumped hydro, hydrogen appears expensive for 2 to 8 hour use cases and even single day storage, as it can’t compete with their efficiency or fast ramp cost without elevated revenue per MWh. Over longer time windows, large underground or industrial scale tank farms begin to become more compelling on a per stored MWh basis, particularly if the hydrogen supports industrial heat or chemical demand so that the same resource stack serves multiple value streams.

Mechanical storage encompasses several rather distinct technologies. Flywheels offer rapid response and high power density but very low energy capacity, so their euros per kilowatt hour is large but their euros per kilowatt can be moderate. Compressed Air Energy Storage and Pumped Thermal Energy Storage treat storage more like a thermodynamic plant, with moderate capital expenditure per kilowatt and low euros per kilowatt hour if you can use underground caverns or low-cost thermal stores. All have a respective round-trip efficiency band and operating limits.

That install costs tend to be more dependent on civil and balance-of-plant work than on the core machines. CAES might require mined caverns or purpose-built tanks along with gas handling and turbo-machinery, while PTES requires high-temperature thermal stores, heat pumps, and turbines. Flywheels require precision bearings, vacuum systems, and heavy-duty enclosures for safety. Maintenance is more mechanical than chemical. Inspections, rotating equipment overhauls, seal replacement, and, for some high-speed designs, careful vibration monitoring are necessary.

Efficiency is what makes it cost-effective, particularly in areas with flat power prices. Flywheels can achieve 85 to 95 percent round trip and near instantaneous response, so they’re great in frequency regulation and power quality roles where you cherish every lost MWh. CAES variants run from approximately 45 percent for older diabatic plants that combust gas up to approximately 70 percent for advanced adiabatic or PTES designs that recycle heat, placing them between hydrogen and batteries on energy efficiency. Self-discharge behavior differs: flywheels lose energy quickly over hours, while CAES or PTES can hold charge for days with low loss, which must be quantified over 1 day, 1 week, 1 month, and 1 year for an apples-to-apples comparison.

Compared to chemical and hydro-based counterparts, mechanical storage still frequently prevails in high-cycle, high-power applications where immediate response (some flywheels respond in milliseconds) and enduring mechanical life are more important than dense energy storage. It can fall short for long-term storage when you extend duration well beyond the design sweet spot because scaling tanks, caverns, and thermal stores is not always linear in cost. In both cases, investors must verify not only LCOS but also service stacking potential, including how much 10%/50%/100% output response times align with grid-service regulations and if cost projections are based on realistic techno-economic analyses, like 60 MW, 480 MWh benchmark plants.

Renewable storage costs now follow global trade flows, policy shifts, and demand cycles. For plant and facility teams, this implies project budgets for solar-plus-storage or grid support can swing rapidly. Humidity-critical loads might experience vastly different economic scenarios depending on the region.

Storage prices remain driven primarily by materials and manufacturing trends. In 2024, global battery prices fell to approximately $165 per megawatt-hour, a 40% decrease from $275 per megawatt-hour in 2023, primarily as a result of increased production volumes, weaker demand in certain markets, and improved cathode chemistry design. In Saudi Arabia, India, and China, panel and battery prices dropped to between one-third and one-half of last year’s prices, which drags turnkey pricing down for utility-scale projects that supply big plants.

Interruptions still stung. Port congestion, export controls on lithium or nickel, or plant shutdowns can delay containers of cells, inverters, and transformers. This can make EPCs add risk premiums. That manifests itself in every line item, from balance-of-plant steel to the dehumidifiers safeguarding battery rooms and inverter halls.

Stable sourcing of lithium, nickel, copper and high‑grade steel mitigates this risk. Other owners now favor regional cell factories and local enclosure builders to reduce lead time, lock in quality, and keep service parts close. It enables you to pull HVAC and humidity packages that meet local fire and corrosion protection codes and source compliant components more easily.

Logistics continues to be the silent but potent cost driver. Heavy battery containers, large transformers and HVAC skids require special trucks, cranes and even route upgrades. Every additional transfer, laydown yard or climate controlled warehouse adds cost per MWh, particularly for isolated industrial locations.

Local rules can swing storage CAPEX by double-digit percentages. Tax credits, feed-in tariffs, and rebates trim effective dollars per kilowatt-hour when they apply to both storage and paired solar. In markets with layered incentives, solar plus storage can come in around or under fossil costs. This is evidenced by projects in the $104 per megawatt-hour range in regions near Las Vegas.

Permitting and safety regulations contribute soft costs. Adherence to fire codes, seismic rules, and environmental impact reviews can necessitate deep modeling, extra engineering time, and additional systems (e.g., advanced fire suppression and tight humidity control). That pressure, in turn, has pushed the industry to safer designs. Grid-scale fire risk is believed to have declined by nearly two orders of magnitude over the previous 5 years, aided by improved enclosure design and more stable indoor climate management.

Local content rules can drive costs higher in the near term if domestic manufacturing is still ramping, but plant the roots of future cost declines as new plants scale and shipping distances shorten. For internal planning, a lot of operators now maintain a modest table of policy-driven adders by country or region, benchmarking tariff exposure, incentive stacks, and permitting timelines to decide where to locate storage-intensive manufacturing.

Integration cost depends on the grid you plug into. A dense, modern network with spare capacity and digital controls can capture storage with less rework, while weak substations or long radial feeders require upgrades that add as much as the battery block itself.

Most areas still require new lines, transformers and protection schemes to accommodate storage at scale. Those upgrades are capital-heavy but can unlock broader savings, including lower losses, more stable voltage for sensitive industrial tools, and smoother integration of large humidity-controlled facilities that run on solar-plus-storage.

Contemporary, flexible grids featuring smart inverters, real-time control, and common interconnection rules typically experience reduced dollars per kilowatt integration costs. They open more value streams, such as frequency response and peak clipping, which helps justify better balance of plant, including strong HVAC and dehumidification.

Developed markets generally have pricier labor and land with more defined regulations. Many emerging grids encounter more affordable labor but greater upgrade requirements. At the same time, global learning curves are steep. Battery costs fell 40% last year and could drop another 22% in a year. The physical footprint halved in one year, and global solar plus storage is now a realistic fossil replacement in many regions, especially where industrial loads can accept flexible, well managed operation.

Storage isn’t simply a €/kWh or $/kWh line item. It resides at the intersection of renewables, grid stability, and long-term risk, and a good deal of that value never appears in a basic cost table.

Storage flattens the delta between flexible supply and inflexible demand. When wind and solar output fluctuate, storage can charge within a few minutes and discharge in seconds, sparing system operators the fast-start gas units, reserve margins, and redispatch costs that instability brings.

It reduces blackout risk and peak stress. Four-hour storage can ride through evening peaks, sustain mission-critical loads through faults, and prevent sags that shut down industrial drives and cleanroom equipment. This “insurance” frequently counts more for a plant than the sticker storage rate.

First, storage provides accurate frequency control. Batteries can respond in under 1 second, so markets pay a premium compared with slower gas turbines. This regulation revenue is a huge chunk of the economic argument in lots of grids.

Not all storage is created equal here. Lithium-ion excels at rapid response and short-duration peaks. Pumped hydro manages larger bulk shifts but is less rapid. Long-duration options, such as flow batteries or compressed air, add depth but perhaps cannot keep up with batteries on ultra-fast control.

Storage reduces exposure to imported gas, oil, or coal and to price spikes in global fuel markets. Combined with local solar and wind, it allows sites and grids to operate more off local resources, with fewer “imported” kWh when prices spike.

Industrial users view this as hedge value. A plant that stores inexpensive off-peak power or excess on-site solar has more stable energy expenses and less downtime risk when the grid is stressed.

Countries with high fuel import bills stand to gain most here. For example, island systems, fuel-importing regions in Asia, and parts of Europe that rely heavily on gas pipelines.

As wind and solar provide a higher portion of power, storage is a crucial resource to maintain minimal curtailment and high renewable penetration. The economics of storage follow suit, as each additional megawatt-hour shifted can displace fossil output and avoid emissions fees or carbon credit purchases.

Today, installing 1 MW of storage power capacity continues to displace under 1 MW of gas generation, and as more storage is installed, the value of each additional unit tends to decline. Longer storage durations exhibit more marginal gas displacement than short-duration systems, which is why the industry is racing past four-hour batteries, even though some four-hour systems have already hit levelized costs under $100 per MWh in some markets.

From a systems perspective, battery storage allows us to utilize existing assets more effectively. It absorbs excess from wind and solar farms, cuts ramping on gas plants, relieves line congestion and can defer or eliminate new transmission and peaker plants. That means lower capital lock-in around fossil units and more room to meet stricter air and health standards.

The problem is price. To truly support deep decarbonization and displace dispatchable fossil plants, grids need cheaper long-duration storage that remains economic over many hours or days, across many years of cycling.

Full renewable power means the grid has to meet peak load every single day with wind, solar, and storage, along with a reserve margin for safety. That is a capacity and cost challenge, not a policy objective. In big systems such as the US, research indicates this requires a massive expansion of generation and storage, with significant impacts on electricity costs and on how plants operate their loads and HVAC systems.

The cost side is grim. One study estimated a 10-year transition to 100% renewables at roughly $1.5 trillion for new wind and solar capacity alone. Other, more recent, estimates reveal average annual spend closer to USD 423.9 billion. At system level, power prices in a 100% renewables mix land in the range of USD 150 to 300 per megawatt-hour, up from about USD 104.8 per megawatt-hour in 2017. If policy rules restrict “low-carbon” to renewables, excluding other sources, total policy costs increase by approximately 10 to 62%. That gap is significant for energy-intensive sites operating paint shops, cleanrooms or massive dehumidification systems 24/7.

Storage is the big X factor. Solar just works in the day. Wind tends to blow more strongly at night. To maintain a clean renewable grid, one U.S. Study references around 900 GW of battery storage, which can bring total price tags close to $4 trillion. Other studies claim that rapid cost declines in solar, wind, and lithium-ion batteries, coupled with the spiraling costs of fossil fuels, can still render the transition low cost. In reality, actual cost will fall between these perspectives and will vary according to how each area configures its mix, grid connections, and demand-side management.

A cost-aware roadmap helps plant teams align with this transition. Key steps include tracking long-term power price paths, not just short-term tariffs, mapping critical loads like dryers, ovens, and dehumidifiers that need tight, stable supply, adding load-flexible assets such as thermal storage, process scheduling, and variable-speed drives, and choosing humidity control that holds setpoints with less kWh per unit of water removed. High-efficiency dehumidifiers, heat-recovery coils, and smart controls reduce peak draw and total energy consumption, which mitigates the impact of higher MWh prices in a 100% renewable future.

Forecasting future prices is about interpreting unambiguous signals from existing cost curves and actual deployment, not just from long-range models. For plant teams who plan 10 to 20 year assets, what matters is how fast batteries, power electronics, and control systems move down the cost curve as factories scale and designs improve.

A lot of the cost studies for solar PV and storage ended up way too pessimistic. Had we known then what we know now, we would have made very different predictions. Actual learning rates exceeded what models assumed. We now see the same pattern in clean firming capacity, which includes grid-scale batteries that back up wind and solar for industrial loads. If your internal business case uses 3-year-old cost curves, you may understate how cheap storage will be by the time a project goes full bore.

A lot of projections still lean on outdated inputs: fixed learning rates, static soft-cost shares, and even a single global cost of capital. In reality, capital costs for a 100 MWh system in Europe, East Asia, and Africa can vary by a few points. That gap by itself can shift levelized cost of storage by tens of percent. If your company operates multi-plant portfolios across regions, you require price forecasts that disaggregate technology cost decline from local finance and permitting risk.

Innovation is already driving prices down more quickly than most scenarios. By 2035, one prediction forecasts LCOE reductions of around 30% in solar, 25% in battery storage, 23% in onshore wind, and 20% in offshore wind. These figures could still be conservative if learning rates remain elevated and if battery and PV manufacturing overcapacity continues to apply margin pressure. Overcapacity, improved pack designs, increased cycle life, and more intelligent control software all drive down the cost per kWh of usable lifetime. For an industrial campus, that translates to more hours of dependable low-cost electricity for the identical capex.

A straightforward chart or timeline of anticipated storage price declines, linked to current real bids and contracts, assists plant managers in timing investments and missing delays induced by stale cost assumptions. Old thinking can stall projects that are already cost‑competitive, even while markets are poised to construct tomorrow’s energy system with today’s tools.

Renewable storage costs continue their fast-paced advance. Costs plummet. Design improves. Risk seems less each year.

Plant teams now face more true tradeoffs. Grid battery banks for peak shaving. Short hour packs for solar. Long hour storage for wind. Smart-controlled hybrids. All routes have compromises, but the voids become increasingly defined.

Low storage cost is about more than just slashing bills. It keeps plants online in storms. It reduces fuel consumption. It assists in striking carbon targets that boards nowadays monitor closely.

Next step remains straightforward. Map your load, peaks, and outage pain. Then fit a storage path to that actual pattern. If you desire a deeper dive into your location, contact Yakeclimate and we can talk through the numbers with you.

Storage costs are a function of technology type (batteries, pumped hydro, hydrogen), system size, raw material prices, project location, grid connection, and financing terms. We find that policy support, supply chain efficiency, and installation labor strongly impact final cost per kWh stored.

Lithium-ion batteries are typically the most economical for short duration storage, which lasts up to 4 to 6 hours. For long-duration or large scale projects, pumped hydro can come out cheaper over its lifetime. Which option is best depends on project needs, site conditions, and grid requirements.

Storage may drive up project costs in the near term. It ultimately tends to reduce system costs. It minimizes wind and solar curtailment, sidesteps cost peaking generation and enhances grid stability. These advantages can assist in constraining or decreasing electrical energy prices over time.

Costs differ because of labor rates, permitting regulations, taxes, land costs, grid interconnection fees, and local supply chains. Financing and government incentives matter. Nations with transparent rules and vigorous competition generally see lower total project prices.

Utility-scale lithium-ion battery costs have fallen by over 80% in the last decade. Manufacturing improvements, economies of scale at higher production volumes, and improved system designs fueled this drop. Prices keep declining, but at a slower pace than before because of the maturing markets.

Storage balances wind and solar’s variable output, shifting power to times of high demand. It cuts fossil backup plants, bolsters grid reliability and unlocks more renewables share. Long duration storage is particularly critical for ultra high renewable penetration.

Most analysts anticipate further cost reductions as technology advances and worldwide implementation expands. Battery chemistries will diversify, raw material use ought to become more efficient, and new long-duration solutions will enter the market. Material constraints and policy shifts might impact that speed.

Contact us to find the best place to buy your Yakeclimate solution today!

Our experts have proven solutions to keep your humidity levels in check while keeping your energy costs low.