Building 34, No. 535 Shunfeng Road, Hangzhou, Zhejiang, China

[email protected]

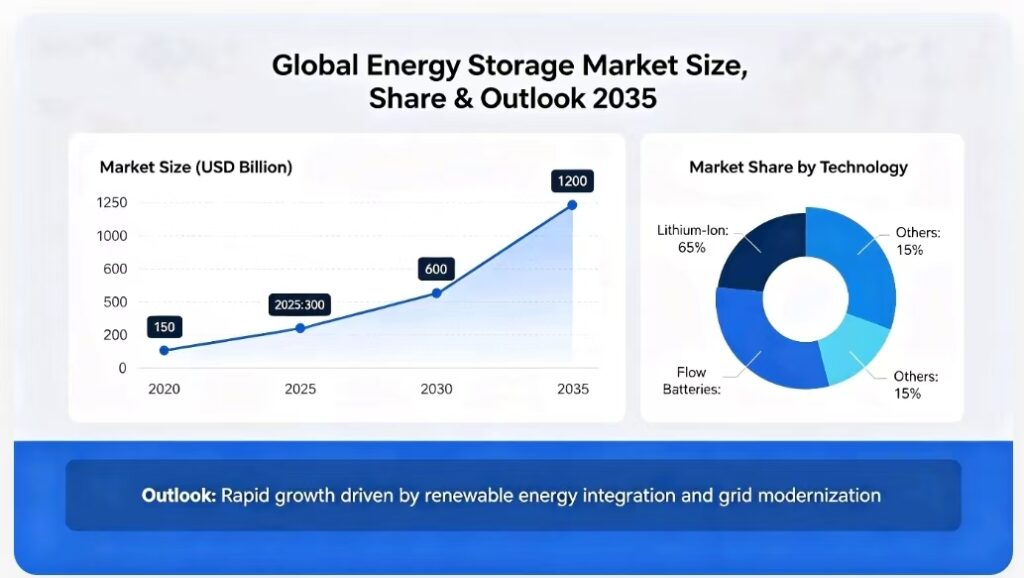

Global energy storage market projections detail anticipated 2023-2030 growth in installed capacity, revenue, and technology mix for grid-scale, commercial, and industrial uses. Projections show healthy demand from renewables, EV charging, and grid stability, with lithium-ion still dominating and more flow, thermal, and hybrid systems in the mix. For plant and facility teams, these projections help schedule power quality, backup, and dehumidification loads around evolving storage assets and duty cycles.

Global energy storage forecasts predict multi-gigawatt annual deployments through 2030 and a global compound annual growth rate of about 14.31% for 2025 to 2030. This growth supports higher renewable shares, more resilient grids, and new service models like Energy-storage-as-a-Service (ESaaS), which many industrial users increasingly view as one way to add resilience without a burdensome upfront capital expenditure.

Storage smooths the mismatch between solar or wind generation and load. It shifts excess mid-day solar into evening peaks and it damps fast ramps when wind speed slows. That’s how grids get to higher renewable penetration without continuous curtailment or backup from gas peakers.

Longer storage duration is a pivotal hinge. Lithium-ion systems now achieve 6 to 8 hours of discharge, making them a head-to-head option against pumped hydro and emerging long-duration concepts to “firm” large solar and wind plants. For instance, a 200 MW solar farm coupled with 800 MWh of storage can push most of its output into the evening peak, rather than spill power at noon.

Curtailment declines as storage absorbs overflow. In high-solar markets, operators are already pre-catching battery over-generation that would otherwise be dumped and then reselling it into peak price hours. That increases the effective capacity factor of the renewable asset and enhances project bankability.

Main solutions in mature markets include lithium-ion containerized systems, flow batteries for 8+ hour profiles, pumped hydro in suitable terrain, and hybrid plants that co-locate PV, wind, and batteries under one grid connection.

Storage is now at the heart of grid modernization plans because it introduces rapid, software-defined flexibility. It can be generation, load, or a grid support device in milliseconds, which legacy assets cannot match at scale.

Battery energy storage systems (BESS) deliver peak-shaving, frequency response, voltage support and spinning-reserve-like services. A 50 MW BESS can react to frequency deviations in less than a second, enabling system operators to maintain frequency within narrow bands even as inverter-based renewables supplant synchronous plants.

Transmission and distribution networks benefit from modular storage located at weak nodes, at substations, or behind industrial meters. This architecture can postpone grid upgrades, reduce congestion, and maintain power quality within process-critical levels for sensitive manufacturing.

Some projects in EMEA and APAC already combine large BESS with high renewables shares to maintain supply stability, even if policy changes stall new solar and wind approvals. All of these places are pursuing aggressive clean-energy goals, and their storage build-out will take off during the 2025 to 2030 period.

National targets for storage and clean power are fueling demand. Governments across India, the UK, US and beyond associate storage with zero-emission targets and climate-risk mitigation, de-risking project pipelines for investors.

Policy instruments span from direct capex assistance to market regulations that reward capacity, flexibility, and ancillary services. When regulations identify storage as its own asset class and enable it to stack revenues, deployment moves quicker.

Renewable portfolio standards, capacity markets, and grid-service auctions all direct investment toward storage as they incentivize resources that are quick and highly available.

| Country/Region | Key Measures Impacting Storage Market Share |

|---|---|

| United States | Investment tax credits, capacity markets, ancillary service auctions |

| United Kingdom | Capacity market, Contracts for Difference, system‑flexibility tenders |

| India | Storage‑linked renewable tenders, viability‑gap funding, peak‑power tariffs |

| Europe (EU) | Green taxonomy, strategic storage targets, transmission‑level tenders |

| Asia‑Pacific | Renewable mandates, grid‑scale storage auctions, industrial tariff reforms |

Storage economics continue to improve as battery pack prices drop and system designs mature. Total installed costs have declined to the point that storage now competes with new thermal peakers in many markets, particularly when value from multiple grid services is stacked.

Increased round-trip efficiencies, extended cycle life, and advanced control software reduce levelized cost of storage. Systems that are over 85 to 90 percent efficient with long cycle counts lower both operating cost and replacement risk over 10 to 15 years.

More affordable hardware leaves room for long-duration storage from cutting-edge lithium-ion and flow systems to thermal or mechanical ideas. These can address multi-hour imbalances associated with large wind or solar fleets.

Recent utility-scale projects often in the USD 150–300 per kilowatt-hour (system level) range back robust new capacity additions in utility, commercial, and to a lesser extent, residential segments.

Electrification of transport, heating and industry drives up power demand and volatility, which increases the requirement for flexible storage. EV charging clusters, electric boilers, and heat pumps contribute new load shapes that grids must wrangle.

It’s a potent battery R&D and scale engine that is the EV market. Improvements in cell chemistry, pack design, and vehicle manufacturing trickle down to stationary storage, reducing costs and expanding technology choices for grid connected projects.

Industrial and residential electrification programs depend on storage to maintain reliable supply when local networks are straining in areas with a lot of rooftop solar or weak feeders, for example. Behind-the-meter batteries, microgrids and ESaaS offerings give facilities more control over power quality and outages.

Among the top drivers connecting electrification to storage growth are increasing peak loads, tighter reliability standards, carbon-reduction policies and hedging power market price spikes.

Emerging storage tech is changing how grids juggle fast-cycling demands, long-duration lulls and seasonal fluctuations. For commercial users, this blend provides the context for power quality, demand charges and carbon profile of each kWh that powers process lines and climate systems such as high-load dehumidifiers.

Non-lithium alternatives advance from pilot to early commercial stage. Redox flow batteries store liquid electrolytes in external tanks, so the energy capacity scales with the volume of the tanks, rather than the size of the cells. Vanadium redox is the most matured, with 8 to 12 hour discharge and over 20 year stack life if tanks, pumps, and membranes are serviced. Zinc-bromine and new organic flow chemistries pursue cheaper and more secure supply chains.

Sodium-based batteries are a second track. NaS systems already serve multi-MW grids with 6 to 12 hour duration and high round-trip efficiency, but operate at high temperature and require rigorous safety engineering. Sodium-ion intends to repurpose much of the lithium-ion production footprint, but at lower energy density, which is a fit better aligned with stationary racks than vehicles. Evolved lead batteries with carbon-enhanced plates minimize sulfation, extend cycle life, and provide a trusted, fully recyclable platform for 1 to 4 hour assignments.

Across chemistries, TRLs span 7 to 9. Flow and NaS already run in utility projects. Iron-air and other metal-air systems aim for 12 to 48 hour LDES with very low material cost. They remain in early field trials. For stationary use, lithium-ion maintains a lead in energy density and supply maturity. Non-lithium alternatives provide extended life at deep cycles, simpler recyclability, or safer thermal characteristics at the expense of larger footprint or narrower operating ranges.

Software now determines how storage truly monetizes and sustains the grid. A battery or hydrogen tank without robust regulatory oversight is wasted metal.

Advanced energy management systems capture high-resolution data on state of charge, temperature, degradation markers, and local load patterns. Cloud analytics then profile price spreads, demand charges, and grid services like frequency control.

On top of that, control platforms run real-time dispatch and co-optimize multiple revenue streams while protecting asset life. They can stack services: peak shaving for a plant, demand response for the utility, and reserve markets in parallel. Digital marketplaces in major regions already allow storage fleets to bid into ancillary services every few minutes with automated trading logic connected to these platforms.

LDES is the fastest-growing segment, expected to grow to around USD 9.5 billion by 2035 at a CAGR of 10.5% from 2026 to 2035. Mechanical storage stands out. Pumped hydro and compressed air energy storage (CAES) are expected to cross USD 8.5 billion by 2035, backed by 79 to 98% cycle efficiencies and decades of field data. They populate big, stable patties requiring daily to weekly shifting, not compact siting.

Thermal storage drives another route. Bricks, sand, rock beds, water, air, or concrete systems retain sensible heat for hours, even days. Combined with electric heaters or heat pumps, they absorb cheap surplus energy and discharge it into district heating grids, industrial drying, or even high-temperature kilns.

For 8 to 24 hour requirements expected to grow at over 10% CAGR through 2035, advanced flow batteries, thermal blocks, and CAES plants manage daily renewables fluctuations. For 12 to 48 hour gaps and storm recovery, iron-air, NaS, and large flow systems aim for deep discharge without cost spikes. Seasonal storage leans toward green hydrogen. Surplus power makes hydrogen via electrolysis, which is stored and later used in turbines, fuel cells, or industrial processes, despite round-trip efficiency of roughly 30 to 45%.

Energy storage expands in all regions globally, not evenly. For plant and facility teams, this lumpy map carves out where supply chains coalesce, where technology costs drop first, and where policy archetypes emerge.

Asia-Pacific secures the biggest share currently, over 46.87% in 2022, and remains the key volume driver. China leads that narrative. As of 2025, it represents approximately 54% of global storage deployments, resulting from rapid grid expansion, increased renewable curtailment and aggressive local planning. Most of it is large front-of-meter lithium-ion, along with increasing pumped hydro and initial thermal pilots connected to industrial and district energy consumption.

North America continues to be that critical second pillar. The US posts a 53% year-over-year install jump in 2025, despite shifting federal rules. Growth is pulled by state clean energy standards, data center loads and corporate PPAs. Europe supplies reliable volumes as it supports wind and solar and fortifies grids against volatility and fuel shocks.

Most mature markets display annual build rates transitioning from hundreds of megawatts to multi-gigawatt levels. That concerns you because gigawatt-scale pipelines drive system and balance-of-plant costs lower and standardize interfaces that connect storage, process loads, and plant-level controls.

Key players span cell OEMs, integrators, and developers: CATL, BYD, LG Energy Solution, Tesla, Fluence, and a wide set of local EPCs. Flagship projects comprise multi-GWh clusters in China’s coastal provinces, large battery hubs in California and Texas, and utility-scale systems in Spain, Germany, and the U.K. For industrial sites, these ecosystems tend to shape the default technology stacks you find in RFPs.

New demand now soars in Asia Pacific excluding China, Latin America, and Africa in particular. A lot of these countries are still industrializing, building new plants and grid connections at the same time, so they can bake storage into the system from day one.

Drivers are obvious. High solar and wind targets, grid congestion near fast-growing cities, and weak legacy networks drive regulators to consider storage both as firm capacity and as a means to smooth voltage and frequency for new industrial zones. That same thirst for stability is why exact humidity and climate control are so important inside the plant fence. Storage and dehumidification often appear in the same capex cycle.

Asia Pacific and North America will remain growth drivers as they invest to modernize substations, expand on-grid capacity, and bring new industrial parks online. Similarly, MEA and C&SA are expected to spearhead thermal storage demand in the long term, frequently associated with process heat, desalination, or district cooling, paving the way for integrated thermal plus air side control concepts at large factories.

Other top emerging countries for future storage expansion are India, Indonesia, Vietnam, Brazil, Chile, South Africa, and Gulf states with robust renewables pipelines. For facility engineers, this is where joint planning of storage, power quality, and humidity-sensitive production lines will transition from pilot to business as usual.

Policy gaps account for a significant part of the regional distribution. Certain markets compensate storage as capacity, some as grid services, and some hardly at all. With explicit revenue rules for frequency response, peak shaving, and resource adequacy in regional markets, project finance costs decline and multi-site industrial portfolios can stack value streams.

Incentives, tariffs, and interconnection rules all alter the calculations. Rapid interconnection queues, equitable demand charges, and acknowledgement of behind-the-meter storage enable plants to firm on-site renewables and maintain consistent indoor climates without over-sizing backup diesel. Badly designed export tariffs, ambiguous metering, or inflexible grid codes stall deployments and leave storage languishing at pilot scale.

China now demonstrates that policy shifts can cut in both directions. With mandatory renewable-storage coupling rules eliminated and revenue structures remaining unclear, project risk increases for 2026–2027, even with robust technical potential. Other regions with thin or stop-start policy support face similar issues: low market liquidity, weak secondary trading, and fewer bankable offtake models.

Energy storage is gaining momentum, and it’s a bumpy road! Policy shifts, grid rules, and weak supply chains still weigh down build-out speed, despite a projected approximately 14.31 percent compound annual growth rate supported by government support for more robust, resilient grids.

Battery and power electronics supply chains remain vulnerable. Most mega-sized systems continue to depend on lithium-ion cells and critical components like lithium, nickel, cobalt, and premium graphite. A disruption in one mining region or one separator plant can set back projects around the world by months, which reshapes cost models and payback periods for industrial users who plan behind-the-meter storage for peak shaving or process backup.

Domestic and regional manufacturing capacity matters for resilience. When more cell, module, inverter, and protection hardware is built closer to demand, project lead times shrink and price volatility calms. It’s a bit like how numerous plants today favor local suppliers for dehumidifiers, chillers, and air-handling units to reduce risk associated with extended ocean routes and customs holdups.

Governments and firms are acting on material security. They finance new lithium and nickel mines, recycle end-of-life batteries, and pilot chemistries with less critical-metal content, such as LFP or sodium-ion. For industrial users, this variety translates into less dependence on one commodity and more secure long-term service agreements.

On the supply side, key initiatives encompass long-term offtake agreements with mines, regional gigafactory joint ventures, recycled-content targets, and digital traceability for ESG reporting. These same tools enable end users to demonstrate environmental stewardship, which now ties tightly to cost management and brand obligation.

Regulation has not caught up with storage. In much of the world, regulations were developed for basic “generation plus load” grids, not for batteries that can serve as load, generator, or grid service within a matter of minutes. These lags hamper market growth in the U.S., China, and other large regions whenever policy transitions alter revenue forecasts midstream.

Old standards tend to get in the way of block stacked value streams. Storage can offer frequency response, peak shaving, backup, and congestion relief, but tariff regulations may identify only one service. If revenue structures are not clear, banks increase their risk premium and many projects die at the model stage.

Compulsory renewable-storage coupling rules and the removal of them create more noise. When coupling is necessary, some sites overbuild storage that is not aligned to real grid demand. As rules roll back too fast, standalone storage projects encounter new uncertainty on their payment.

Faster regulatory adaptation means defining storage as its own asset class, having standard contracts for grid services, clear safety codes, stable compensation schemes, and often with incentives like upfront grants or performance-based payments over years. That provides developers and industrial hosts sufficient comfort to transition from pilot to fleet deployment.

Grid interconnection is now among its most constricting bottlenecks. Storage projects queue up with wind and solar as system operators figure out studies, protection settings, and capacity constraints. These delays can wipe out the advantage of declining hardware costs and incentivize industrial buyers to postpone behind-the-meter options.

Technical hurdles are short-circuit limits, inverter ride-through rules, and concerns about fast ramping on weak feeders. Procedural hurdles are just as hard: different forms, study queues, and opaque timelines across regions. When rules change mid-study, risk jumps anew.

Efficient processes are crucial. Predictable interconnection processes, open queues, pre-defined hosting capacity maps, and standardized contracts can reduce months from timelines. Certain markets have since enabled Energy-Storage-as-a-Service (ESaaS), which allows a third party to own and operate the asset, manage interconnection, and offer services back to the plant on straightforward contracts.

Best practices are early grid impact screening, standardized inverter models and modular system designs, and coordinated planning between utilities, regulators and large industrial users. Combined with transparent revenue rules and targeted incentives, these steps enable both cost reduction and improved environmental performance. Together, they fuel more widespread adoption of storage similar to other efficiency measures such as advanced dehumidification.

The Energy Storage Grand Challenge is a whole-of-government endeavor to develop, scale, and manufacture storage technologies domestically that satisfy all market needs by 2030. It targets long-duration energy storage for multi-hour and multi-day support, crucial to firming wind and solar, stabilizing grids and supporting critical loads in plants and data centers. The DOE ESGC Roadmap, published in December 2020, defines the line of sight from early R&D to full commercial deployment, with clear roles for public agencies, industry, and research labs.

The ESGC roadmap establishes clear targets for long-duration systems by 2030, including installed costs below approximately 50 to 60 USD per kilowatt-hour for long-life stationary systems, round-trip efficiency greater than 70 to 80 percent based on the technology class, and lifetimes exceeding 20 years or 8,000 to 10,000 cycles for grid-scale applications. It ties those targets to real use cases: 10 to 100 plus hour storage for bulk shifting, firm capacity, and resilience services.

Since 2020, cost curves for several LDES options have begun to bend down, aided by scale-up and design simplification. Flow batteries are migrating from niche pilots to multi-MWh systems. Thermal and mechanical storage pilots are now receiving 2024 funding support, including approximately $100 million USD dedicated to various LDES pilots. These pilots aren’t at full target cost yet, but they’re closing the gap quickly enough for utilities and large industrial users to run real tenders.

Tight energy‑efficiency and performance standards contribute directly to this trend. Definite minimum round‑trip efficiency, auxiliary load and standby loss rules drive vendors to snip parasitic loads and tidy up control strategies. For plant engineers, that translates into more predictable operating costs and superior asset planning over 15 to 20 years.

Typical ESGC metrics are LCOS (USD/MWh delivered), capital cost per kW and per kWh, round-trip efficiency, cycle and calendar life, response time, availability, and degradation rate. For industrial sites, additional metrics matter: power quality (voltage and frequency support), ability to ride through humidity-induced HVAC upsets, and integration with on-site systems like dehumidifiers and process chillers.

The ESGC additionally advocates for robust domestic production and local supply networks, so storage is not just economical but safe and transparent. This connects to national clean‑energy objectives and energy‑security issues, particularly as LDES capacity expands from a 3.6 billion USD market estimated in 2025 to around 9.5 billion USD in 2035 with a compound annual growth rate of 10.5%.

Policy tools back this shift: production tax credits for cells and packs, grants and low-cost loans for gigafactories, and incentives for local content in public tenders. A few countries combine this with workforce training around battery assembly, power electronics, and system-level integration. This blend can root jobs in areas with large industrial clusters.

Being locally produced decreases shipping risk, shipping lead time, and exposure to geopolitical shocks. It allows tighter feedback loops between cell makers, system integrators, and major purchasers like automotive plants, semiconductor fabs, and pharma sites that require customized backup and power-quality solutions.

Think U.S., EU and China funding cell plants, component factories and balance-of-system suppliers. Several of these programs link funding to environmental and safety standards such as thermal management and environmental control requirements, which lend themselves nicely to precise humidity and temperature control in vast storage halls.

The circular approach is now at the heart of ESGC thinking. Its roadmap identifies high recycling rates, reuse pathways, and sustainable materials as core design goals, not afterthoughts. That means improved collection, cutting-edge sorting and recovery lines, and pack design standards that facilitate disassembly and recycling.

Lead-acid batteries already demonstrate what high-loop efficiency looks like, with recycling rates of over 95% in many areas. That experience is feeding into lithium-ion and new chemistries, where hydrometallurgical and direct-recycling routes seek to reclaim lithium, nickel, cobalt, and other metals with less energy and waste.

Recycling rates that are high help to reduce raw-material demand, minimize the impacts of mining, and stabilize the costs of inputs over time. This aids long-term ESGC goals and 100 percent clean-energy targets that rely on scaling LDES with hundreds of millions in public funding and increasing private capital.

Major battery makers now embrace circular strategies like design for disassembly, take-back schemes linked to product sales, second-life use in stationary storage, and on-site recycling partnerships in close proximity to industrial clusters. For big users like sites that implement tight humidity control to safeguard both storage assets and production lines, these closed-loop models reduce risk and help meet more stringent environmental regulations.

Energy storage is transitioning from a niche to core infrastructure. Annual installs are projected to exceed 100 GW in 2025, utility-scale systems representing roughly 82% of that volume. This scale does more than balance ledgers. It humbly transforms local labor markets, capital flows, and the cost structure of power-hungry plants that operate paint lines, cleanrooms, and drying ovens.

The wave to 92 GW of new non-pumped storage in 2025, 23% more than 2024, means a significant employment draw. Direct jobs appear in project design, EPC work, battery production, thermal solutions, and O&M. Indirect jobs appear in mining, component foundries, power electronics, HVAC, logistics, and site services. For each MW of storage commissioned, several full-time jobs emerge throughout build and a modest but consistent group persists for operations, monitoring, and occasional overhaul.

A lot of areas now support workforce initiatives connected to storage and the general energy transition. In China and the US, where they represent around two-thirds of annual build, with a share of over 50% and 14% by GW, respectively, technical institutes conduct crash courses on battery safety, high-voltage interconnection, and digital controls. Resource economies such as India and Indonesia tie storage to national skilling pushes so local laborers can shift from informal builds into grid-connected projects with extended career trajectories.

Key skills and training needs in the storage value chain include:

For industrial users, this labor shift is important. A plant that combines on-site storage with sophisticated dehumidification requires engineers who know both energy and environment. That mix maintains batteries in a secure moisture range, safeguards switchgear and reduces unexpected downtime. It connects the macro job narrative to day-to-day dependability on the assembly line.

Storage increases the proportion of local, variable renewables that grids are able to accommodate without endangering stability. By time-shifting wind and solar, countries are less exposed to imported fossil fuel and gas price volatility. This is especially important in rapidly growing systems, like China, India, and Indonesia, where demand and climate ambitions grow in tandem.

In practice, storage allows for smaller, more resilient power ‘islands’. Industrial parks sandwich PV, batteries, and surgical HVAC to cruise through grid faults and storms. That blend decreases the reliance on diesel backup, evens out tariff spikes, and helps stabilize long-term energy costs for process lines that cannot halt such as pharmaceutical drying, food packaging, or electronics curing.

Some nations already connect storage to security strategy. China deploys large-scale batteries to enable high renewable penetration in coastal and inland provinces and builds a domestic supply chain that anchors manufacturing jobs. The US supports storage via tax credits, with projects sited near load centers to maintain vital manufacturing clusters online during grid strain. Island and quasi-island systems, from Indonesia’s archipelago grids to remote mining hubs, deploy storage to reduce fuel imports and maintain power quality within tight tolerances required for sensitive machinery and climate-controlled environments.

There’s another ripple: seed capital is flowing at a rapid pace from legacy thermal plants to storage, next-gen inverters, and grid-forming assets. Investors are growing into long-duration systems, co-located solar-plus-storage, and behind-the-meter projects at plants eager for demand-charge cuts as well as higher resilience. While policy shifts in the US and China could slow its growth rate in 2026, the long-term flow of funds still leans toward flexible capacity rather than new baseload.

Large deals highlight this trend and shape cost curves:

| Year | Investor/Acquirer | Target/Project Type | Region |

|---|---|---|---|

| 2023 | Global infra fund | 1+ GW utility‑scale battery portfolio | North America |

| 2023 | Asian utility | Grid‑scale storage developer | Southeast Asia |

| 2024 | EU energy major | Solar‑plus‑storage pipeline | Europe |

| 2024 | Tech manufacturer | Cell and BESS gigafactory expansion | Global |

These investments boost local economies by attracting construction companies, electrical contractors, HVAC and dehumidifier vendors, and digital providers. Economic multipliers are significant. Each unit of storage spending ripples through metals, electronics, civil works, transport, and O&M. To industrial plants, the impact appears as more consistent power rates and new service propositions, like shared warehousing hubs with on-demand climate control that serve both grid demands and tight in-plant humidity requirements.

Global energy storage is at a genuine turning point. Growth goes into grid projects, EV packs, and behind-the-meter systems. Figures in recent market projections confirm this with distinct new capacity year-over-year increases.

You see new chemistries transition from pilot lines to full plants. You watch more long‑duration projects transition from slide decks to live grid assets. Policy, price drops, and supply chain shifts all drive in the same general direction.

Huge gaps still remain. Initial price, extended lead times, and grid regulations continue to hinder initiatives. Every new large-scale site provides engineers new data and reduces risk for the next.

To size or test storage for your own plant or process, get in touch with the Yakeclimate team for a deep dive on your case.

The global energy storage market is expected to see rapid growth in the next 10 years. Declining battery costs, climate goals, and grid upgrades are significant factors. Storage is becoming essential for reliable, low-carbon power systems around the world, and analysts forecast robust double-digit yearly growth.

Lithium-ion batteries currently reign for cost, maturity and scalability. Long-duration solutions such as flow batteries, thermal storage and green hydrogen are garnering attention. Future market leadership will therefore be a mix of short- and long-duration technologies for specific grid and industry needs.

Regional growth varies depending on policies, renewable targets and grid needs. Asia-Pacific tops deployment again. Europe surges with ambitious policies. North America expands with market reforms. Growth occurs in developing markets where solar and wind capacity is expanding rapidly and where there is a push for more resilient power systems.

Main challenges are significant initial costs, undefined marketplace regulations, permitting bottlenecks, and supply chain vulnerabilities. In certain areas, antiquated regulations do not compensate storage’s comprehensive services. Solving these challenges is key to scaling storage and attracting long-term private investment.

Energy storage is a ‘grand challenge’ for it must provide dependable, cost-effective, low-carbon flexibility at scale. It backs up variable renewables, stabilizes grids and minimizes fossil backup. Cracking this puzzle unlocks further emissions abatement across power, industry, buildings and transportation.

Storage generates jobs in manufacturing, construction, and services. It can reduce system costs by postponing grid upgrades and mitigating peak power prices. It underpins new business models — virtual power plants, prosumer markets — sculpting energy and infrastructure investments of the future.

Here’s what investors and businesses can take advantage of by honing in on regions with defined policies, grid-hungry needs and strong renewable pipelines. Opportunities exist across project development, technology supply, software and services. Knowing your local regulations and revenue streams is key to managing risk and returns.

Contact us to find the best place to buy your Yakeclimate solution today!

Our experts have proven solutions to keep your humidity levels in check while keeping your energy costs low.